Regulatory reforms, infrastructure investment, and evolving capital market instruments are reshaping how developers finance real estate projects—and where the next wave of demand will emerge.

Real Estate Funding · REITs · SM REITs · Urban Development

The Macro Context: Infrastructure as a Demand Engine

India’s real estate sector has historically tracked two primary variables: interest rates and income growth. In 2026, a third variable has emerged with structural permanence — public infrastructure investment.

With the government committing 12.2 lakh crore in capital expenditure for FY 2026-27, the geography of real estate demand is being actively redrawn.

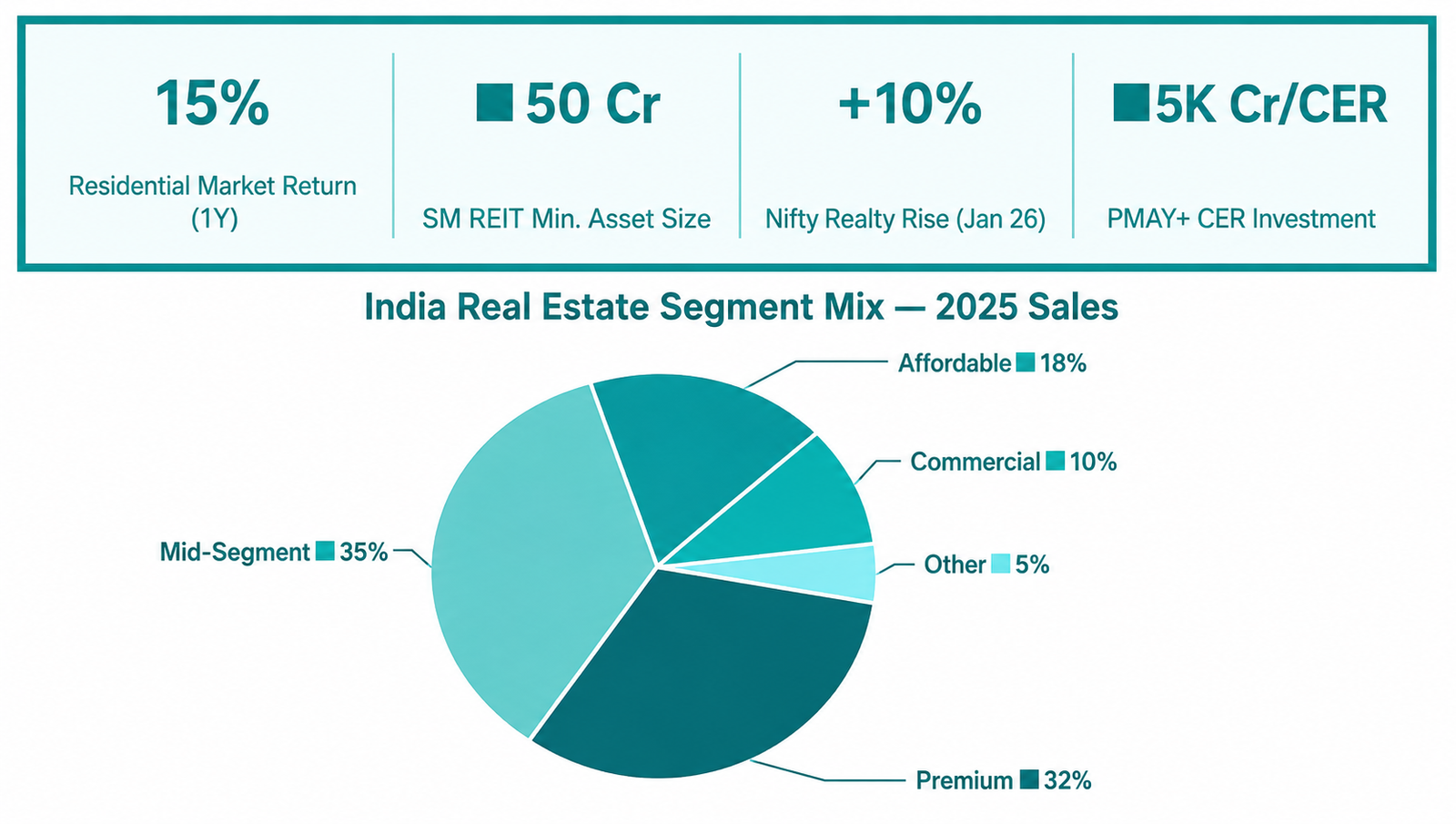

The development of seven high-speed rail corridors, the creation of City Economic Regions with dedicated investment of ₹5,000 crore per CER, and intensified urban infrastructure in Tier 2 and Tier 3 cities are generating demand signals in markets that institutional investors previously overlooked.

For developers and financiers, this represents a genuine frontier opportunity — provided the underlying deal structuring and funding architecture can keep pace.

The REIT Revolution: SEBI SM REIT Framework

On the regulatory front, the SEBI Small and Medium REIT framework has meaningfully lowered the entry threshold for market participation.

The Securities and Exchange Board of India (SEBI) has reduced the minimum asset size for a REIT from ₹500 crore to ₹50 crore, while a scheme-based structure now allows a single SM REIT to house multiple sub-₹500 crore asset pools.

This significantly expands the investable universe for institutional and sophisticated investors.

Critically, effective 1 January 2026, SEBI classified Mutual Fund and Specialised Investment Fund investments in REITs as equity-related instruments.

This reclassification introduces much-needed secondary market liquidity into the REIT space, making these instruments more attractive to a broader base of domestic institutional investors.

Market analysts expect this shift to increase demand for stabilized commercial real estate assets that sponsors can pool and offer as a regulated investment product.

Residential Real Estate: Demand Without Incentives

The Union Budget 2026–27 notably lacked direct demand-side incentives for residential real estate — no enhanced tax deductions for home buyers, no GST relief for developers, no new affordable housing mandates beyond the continuation of existing PMAY allocations.

Yet the residential segment has shown remarkable resilience.

Nifty Realty constituents collectively rose over 10% in early January 2026, and the residential market delivered an estimated 15% total return in the preceding twelve months — outperforming broader equity indices.

Industry experts ground this performance in structural demand from an urbanizing middle class and in the growing expectation that infrastructure investment will improve liveability and connectivity in target markets.

Construction Finance: The IRGF Effect

Budget 2026–27 introduced the Infrastructure Risk Guarantee Fund, which market participants have received as a structural positive for construction lending—the segment of real estate finance most prone to disruption.

By partially de-risking construction-phase borrowing, the IRGF expects to improve credit flow from banks and NBFCs to developers, targeting affordable and mid-segment housing in particular.

Industry participants, including the CMD of Sumadhura Group, have noted that credit guarantees during construction may enhance funding continuity and support timely delivery — factors that directly influence buyer confidence and project viability.

For financial advisors and lenders, this mechanism creates a new toolkit for structuring construction finance transactions.

The Leverest Perspective

Real estate and corporate funding in India have evolved far beyond simple bank loans. Today’s landscape demands a sophisticated mix of capital solutions, ranging from traditional project finance to specialized structured debt.

At Leverest Financial Services, we help developers and businesses structure the right capital solutions for complex projects—combining financial advisory, capital sourcing, and deal structuring expertise.

By connecting clients with banks, NBFCs, and alternative investment funds, we ensure that every project receives a financing structure aligned with its scale, risk profile, and growth potential.

Our practice provides clients with a comprehensive suite of financial services, ensuring every project—from greenfield developments to brownfield expansions—receives optimal support.

Leveraging our deep relationships with banks, NBFCs, and AIFs, we provide the deal expertise and execution power needed to navigate the modern financial market.

India’s real estate sector is entering a new financing era—one driven by infrastructure investment, evolving regulatory frameworks, and deeper institutional participation.

For developers and investors alike, navigating this landscape requires not only capital but the right capital structure.

As the market evolves, financial advisory firms will play an increasingly critical role in aligning projects with the most efficient sources of funding.