India’s monetary landscape has undergone a decisive transformation. The Reserve Bank of India’s Monetary Policy Committee (MPC), under Governor Sanjay Malhotra, has delivered a cumulative 125 basis points in rate cuts, bringing the benchmark repo rate down to 5.25% as of February 2026 — one of the most aggressive easing cycles in recent memory.

For Indian businesses navigating capital structure decisions in 2026, understanding the mechanics of this rate cycle is not merely an academic exercise. It is a strategic imperative.

With the Standing Deposit Facility (SDF) now at 5.00% and the Marginal Standing Facility (MSF) at 5.50%, the 50-basis-point LAF corridor is the tightest it has been in 10 years — signalling a deliberately accommodative monetary stance. The RBI’s priority is clear: transmit the rate reduction to the real economy as efficiently as possible.

Background and Industry Context

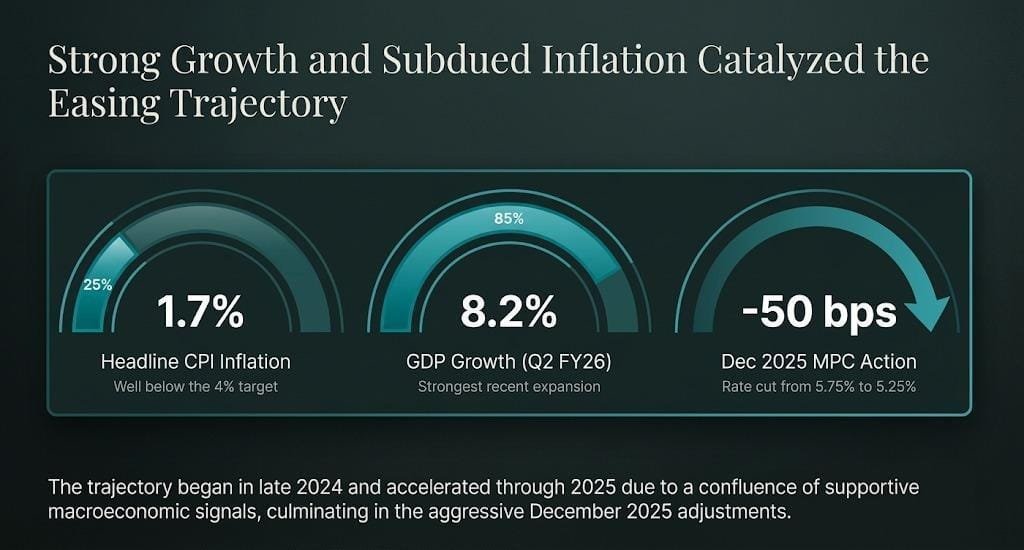

The RBI’s rate-cutting trajectory began in earnest in late 2024 and accelerated through 2025 amid a confluence of supportive macroeconomic signals.

Headline CPI inflation fell to 1.7% — well below the 4% target — while GDP growth reached 8.2% in Q2 FY26, one of the strongest quarterly expansions in recent memory. The December 2025 MPC meeting alone delivered a 50-basis-point reduction, taking the repo rate from 5.75% to 5.25%.

Concurrently, the Cash Reserve Ratio (CRR) was reduced to 3.00%, and long-term forex buy/sell swap auctions injected USD 15.1 billion in liquidity through December 2025 and January 2026.

Banking-sector NPAs have fallen to a multi-decadal low of 2.5%, and the credit-to-deposit ratio has stabilised at 78%, creating a strong foundation for expanded credit deployment.

Critically, all new floating-rate loans to retail and MSME borrowers must now be linked to an External Benchmark Lending Rate (EBLR) — typically the repo rate — making policy rate changes directly visible in lending costs within the quarterly reset cycle.

Key Developments and Data

Monetary Policy Transmission: Near-Complete

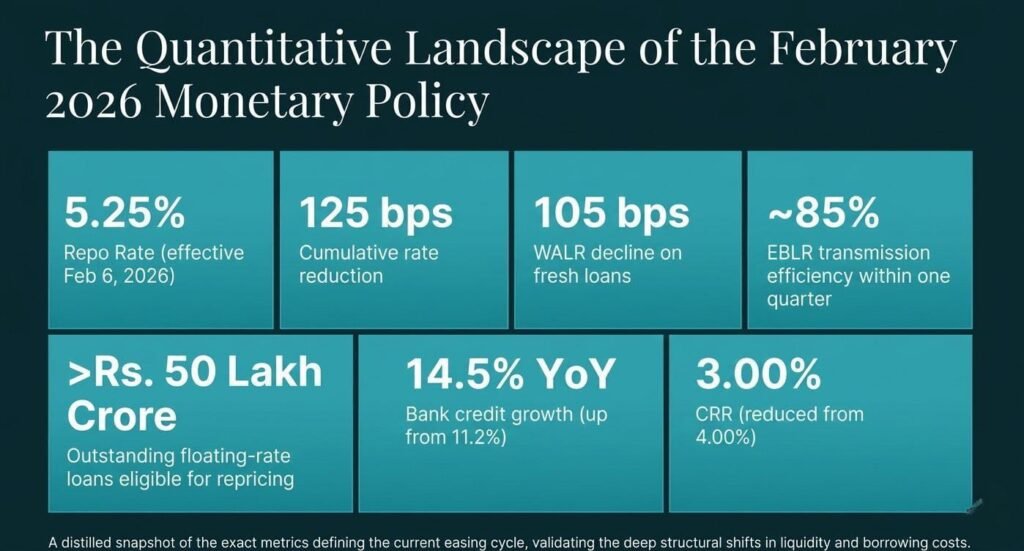

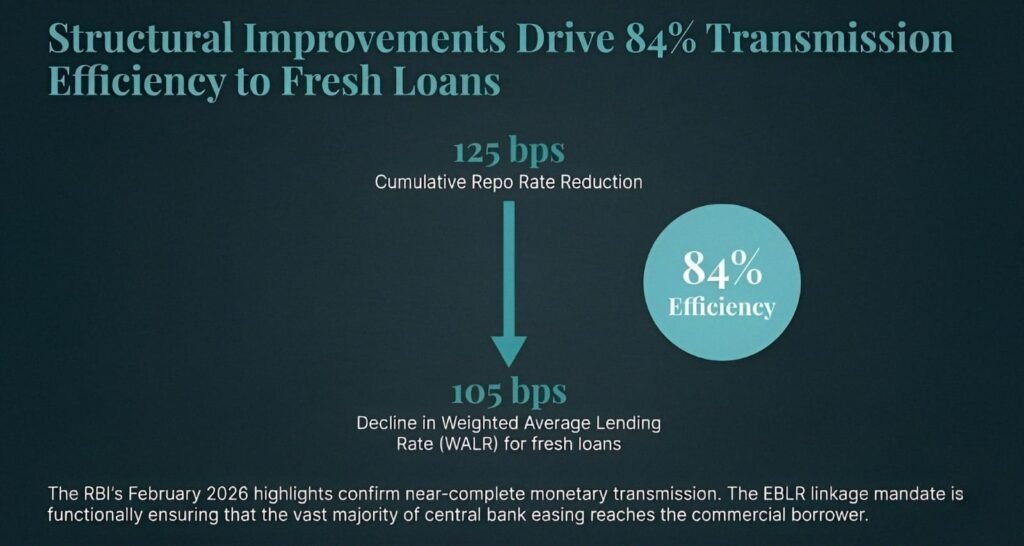

The RBI’s February 2026 monetary policy highlights confirm that the weighted average lending rate (WALR) of scheduled commercial banks declined by 105 basis points for fresh loans in response to the cumulative 125 bps repo rate reduction.

This near-complete transmission (approximately 84%) reflects the structural improvements enabled by the EBLR linkage mandate.

- Repo Rate: 5.25% (effective February 6, 2026)

- Cumulative rate reduction since easing cycle began: 125 basis points

- WALR decline on fresh loans: 105 basis points

- EBLR transmission efficiency: approximately 85% within one quarter

- Outstanding floating-rate loans eligible for repricing: over Rs. 50 lakh crore

- Bank credit growth: 14.5% YoY as of December 2025, up from 11.2% in December 2024

- CRR: 3.00% (reduced from 4.00% in 2024)

Market expectations currently price in one additional 25-bps cut in the near term, contingent on inflation remaining below 3%, potentially bringing the repo rate to 5.00% by mid-2026.

Impact on Indian Businesses and Borrowers

Reduced Borrowing Costs: For EBLR-linked borrowers, lending rates have adjusted downward within 90 days of each rate action. Average home loan rates fell to approximately 8.10% following the December cut, trimming monthly EMIs meaningfully for mid-income buyers and improving project economics for developers.

Working Capital Efficiency: Lower interest rates reduce the carrying cost of working capital facilities, directly improving operating cash flows for MSMEs, manufacturers, and traders. For a company with Rs. 10 crore in working capital utilisation, a 100-bps rate reduction translates to Rs. 10 lakh in annualised interest savings.

Infrastructure and Project Finance: With long-tenor project loans repricing at more competitive rates, infrastructure developers face a structurally improved financing environment. The combination of lower borrowing costs and the government’s Rs. 12.2 lakh crore capex outlay in Budget 2026 creates a powerful catalyst for project finance activity.

Debt Refinancing Opportunity: Companies carrying high-cost legacy debt originated during the 2022-23 rate-hike cycle should urgently evaluate refinancing. The spread differential between legacy MCLR-linked loans and current EBLR-linked facilities can be 80-150 basis points, representing material annualised savings on large loan books.

Strategic Implications for Financing

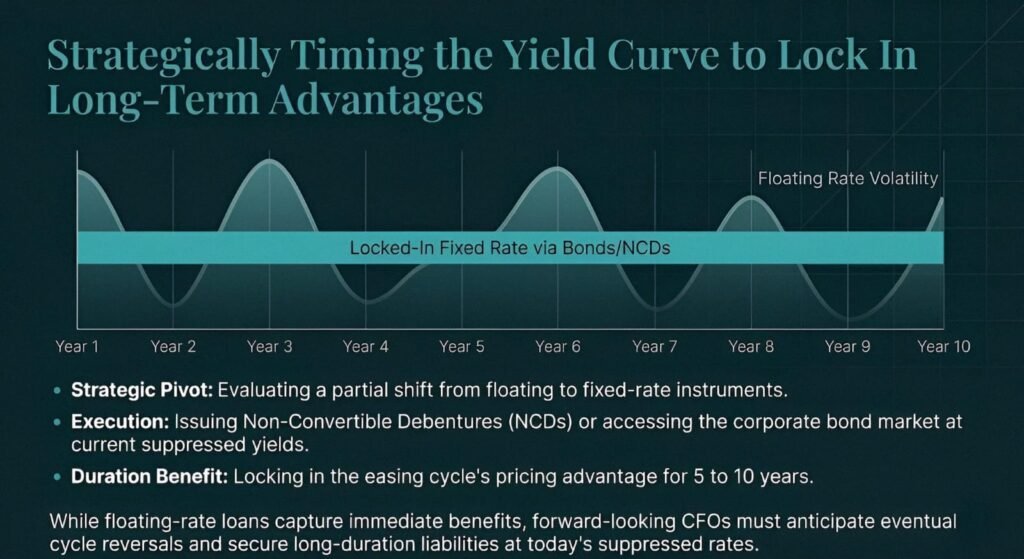

Lock In Long-Term Rates Strategically

While floating-rate loans benefit immediately from rate cuts, CFOs should evaluate whether a partial shift to fixed-rate instruments — before any potential rate cycle reversal — makes strategic sense for long-duration liabilities.

Issuing NCDs or accessing the corporate bond market at current yields locks in the benefit of the easing cycle for 5-10 years.

Accelerate Debt Syndication Activity

The easing cycle has energised India’s debt syndication market. With the banking sector at its healthiest in years and lenders actively seeking quality credit exposure, well-structured syndicated facilities can now be executed at significantly improved pricing and terms compared to 18 months ago.

For borrowers with strong credit profiles, this is an opportunity to negotiate better covenants and extended tenors.

Lock In Long-Term Rates Strategically

While floating-rate loans benefit immediately from rate cuts, CFOs should evaluate whether a partial shift to fixed-rate instruments — before any potential rate cycle reversal — makes strategic sense for long-duration liabilities.

Issuing NCDs or accessing the corporate bond market at current yields locks in the benefit of the easing cycle for 5-10 years.

Accelerate Debt Syndication Activity

The easing cycle has energised India’s debt syndication market. With the banking sector at its healthiest in years and lenders actively seeking quality credit exposure, well-structured syndicated facilities can now be executed at significantly improved pricing and terms compared to 18 months ago.

For borrowers with strong credit profiles, this is an opportunity to negotiate better covenants and extended tenors.

Refinancing and Capital Structure Optimization

For leveraged corporates, the rate cut creates a window for comprehensive capital structure review — reducing overall debt cost, extending tenor profiles, and improving DSCR (Debt Service Coverage Ratio).

This is particularly relevant for infrastructure developers and real estate companies with long-dated debt obligations.

Expert Perspective

At Leverest Financial Services, we view the current monetary policy environment as one of the most constructive backdrops for corporate debt restructuring and new fundraising that India has witnessed in over a decade. However, rate tailwinds alone do not determine financing outcomes.

Successful debt syndication in this environment requires precise credit positioning — ensuring lenders see not just a lower rate environment, but a borrower with strong cashflow visibility, transparent governance, and a coherent repayment strategy.

Our advisory approach combines deep capital market intelligence with sector-specific structuring expertise, helping corporates optimise access to both bank credit and non-bank financing channels.

84%For businesses evaluating working capital enhancement or long-term project finance, now is an opportune moment to engage with a seasoned financial advisor.

The cost of delay in this rate environment can be measured in basis points foregone on every rupee of outstanding debt. Explore Debt Syndication | Working Capital Finance solutions at Leverest.

Conclusion

The RBI’s decisive monetary easing has created a generational opportunity for Indian businesses to optimize their cost of capital. With the repo rate at 5.25%, EBLR transmission functioning effectively, and the banking sector health at multi-year highs, the financing landscape is genuinely supportive.

Forward-looking CFOs and business owners who act decisively — restructuring, refinancing, and raising capital in the current window — will gain a structural competitive advantage that outlasts the rate cycle itself.