Beyond the Single Lender: Building a Credit Stack That Scales With You

The CFO who realized her credit stack was an accident

A few months ago, the CFO of a fast-scaling consumer business sat across from us and laid out her balance sheet.

Six lenders. Eight facilities. Not one of them chosen on purpose.

One came in because the founder’s CA had a contact. Another said yes when nobody else would. A third was inherited from the parent company two acquisitions ago. The rest had drifted in over the years — fastest sanction, longest relationship, easiest renewal.

She wasn’t running a credit structure. She was running a museum of past urgencies.

Most companies don’t choose their lenders. They accumulate them.

That’s the quiet truth across Indian SMEs and mid-market businesses. The credit stack gets built reactively — one cash crunch, one new project, one bridge loan at a time. By the time someone finally looks at it from above, it’s a patchwork stitched together by who said yes first, not who fits best.

The shift is happening underneath

Indian households are quietly moving their savings out of bank deposits and into equities and mutual funds. Which means banks are now funding the same loans with more expensive money. At the same time, the MSME credit gap remains enormous, and service businesses and women-owned firms are even further from the formal credit system than the headlines suggest.

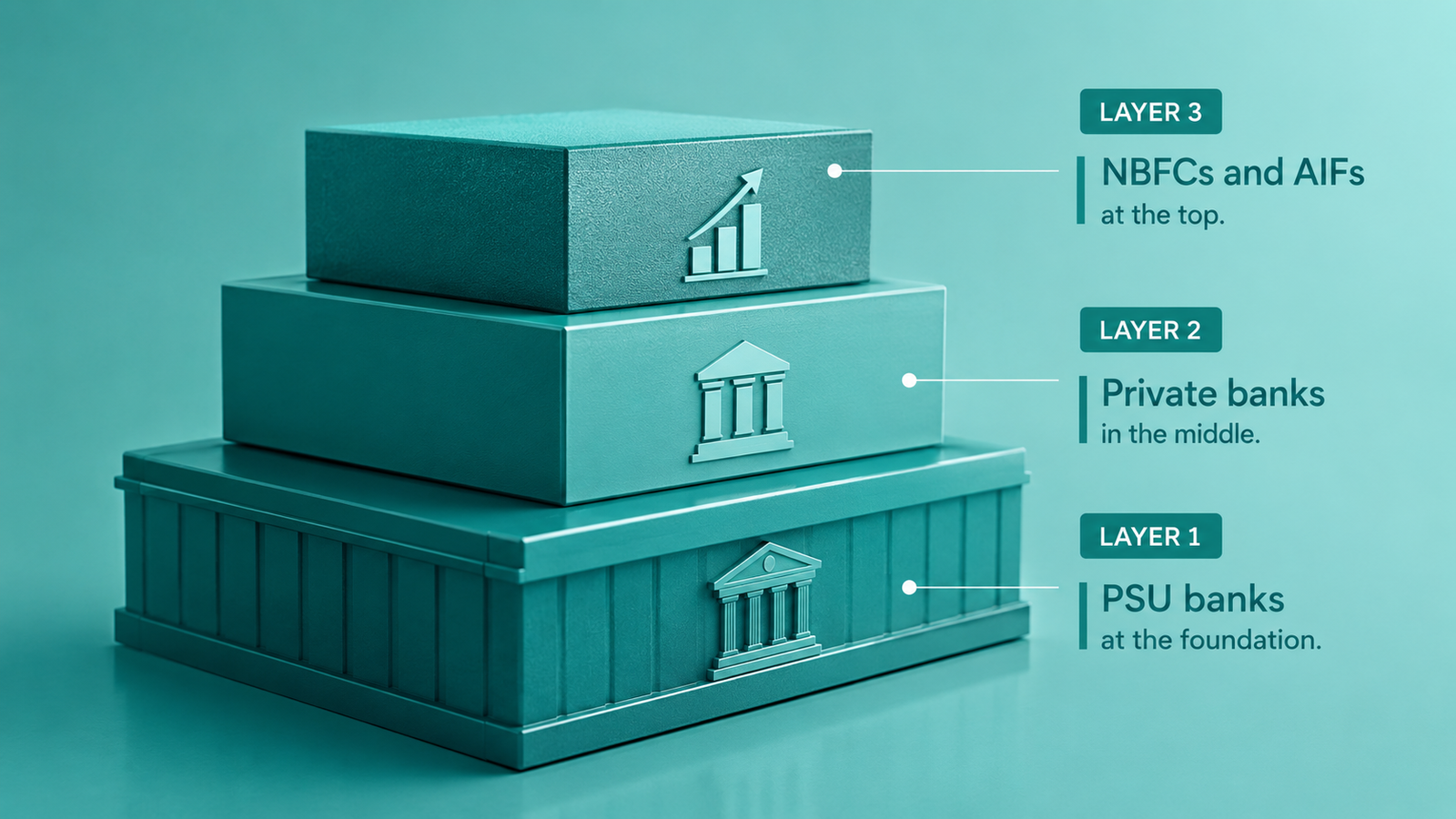

How we advise clients to think about the three layers

When we sit down with a CFO to redesign their credit stack, we work through it in three layers — each doing something the other two cannot.

Layer 1 — PSU banks at the foundation. This is where we anchor the cheapest, longest-tenor capital. Term loans, working capital limits, and government-backed schemes like CGTMSE. They’re slow and documentation-heavy, but the regulatory weight matters when credit ratings are being assessed — and the pricing remains unmatched. We typically advise clients to size this layer for stable, predictable needs that can absorb a longer sanction cycle.

Layer 2 — Private banks in the middle. This is the layer we use for speed without giving up bank-level pricing. Structured working capital, trade finance, forex lines. Their underwriting is faster, their technology is sharper, and they sit in the right zone for transactions where turnaround is part of the deal. We deploy this layer for the needs that PSU banks are too slow for, but that don’t need NBFC-level flexibility.

Layer 3 — NBFCs and AIFs at the top. This is where we structure everything the banks won’t touch or can’t move fast enough on. Invoice discounting, supply chain finance, bridge loans, acquisition financing, mezzanine capital, special situations. Disbursed in days, structured around the actual cash flow rather than the balance sheet at rest. We use this layer for time-sensitive, sector-specific, or structurally non-standard requirements — where the right instrument matters more than the headline rate.

The job isn’t to pick one layer. It’s to use all three deliberately, with each carrying the part of the balance sheet it’s actually designed for.