Why This Matters Right Now

India’s MSME credit landscape just shifted — quietly but consequentially.

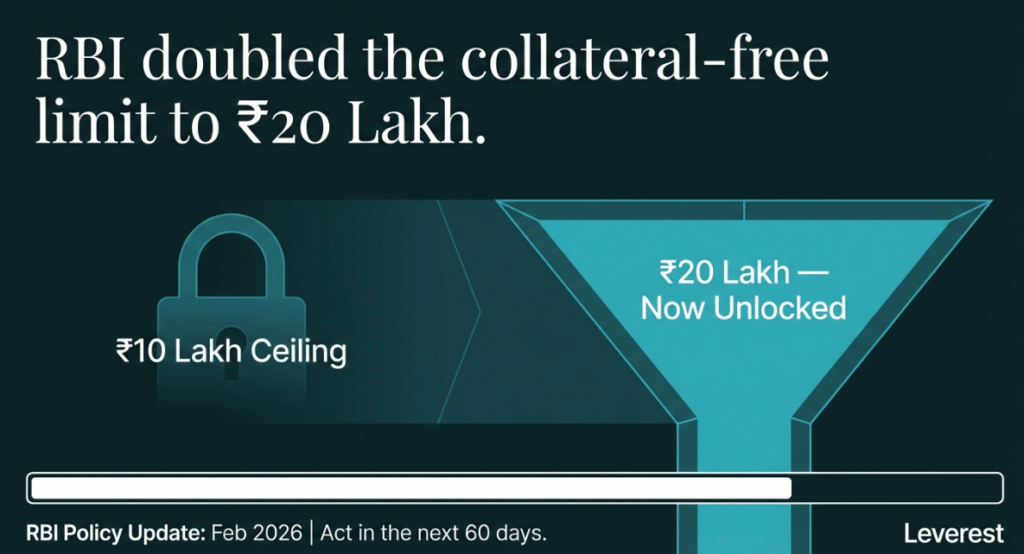

RBI’s revised priority-sector lending circular, issued in February 2026,

lifts the collateral-free lending ceiling for MSME borrowers from ₹10 lakh to ₹20 lakh.

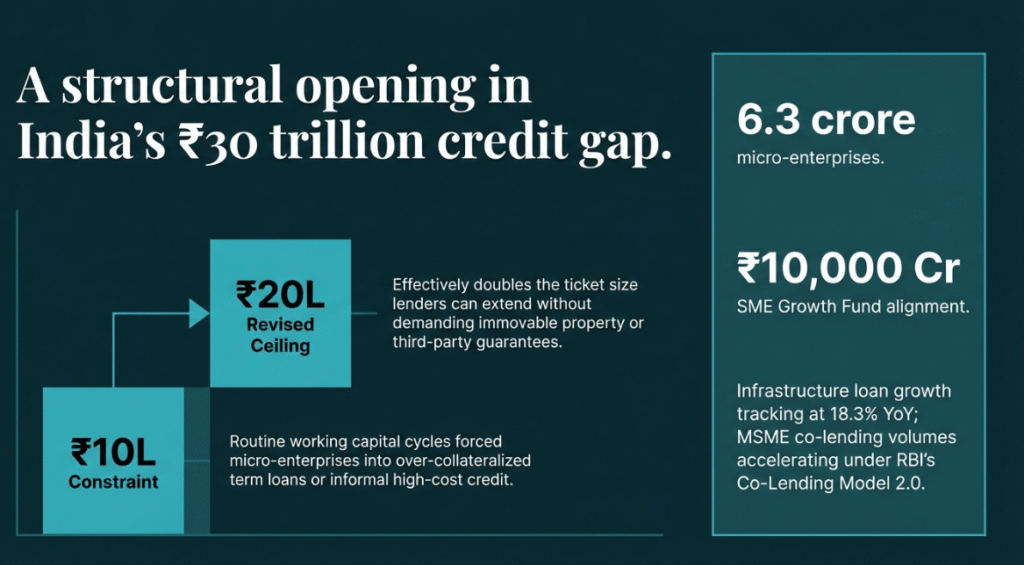

For the 6.3 crore micro-enterprises that make up India’s MSME base, this is not a minor regulatory tweak.

It is a structural opening in a market where the formal credit gap sits at ₹30 trillion.

Banks are reconfiguring their internal credit matrices right now.

Lenders who move first — with clean documentation, structured cash-flow narratives,

and sound borrower profiles — will capture the best rates and the fastest disbursements.

MSME owners who wait for their relationship manager to call

will find themselves competing for the same credit window in an increasingly crowded queue.

The Policy Shift — And What It Actually Unlocks

The ₹10-lakh unsecured lending cap was a significant constraint for micro and small enterprises.

Most working capital cycles — inventory purchases, advance payments to suppliers,

short-term operational buffers — routinely exceed this limit, forcing borrowers into either over-collateralized term loans or informal high-cost credit.

The revised ceiling to ₹20 lakh effectively doubles the ticket size that lenders can extend without

demanding immovable property or third-party guarantees.

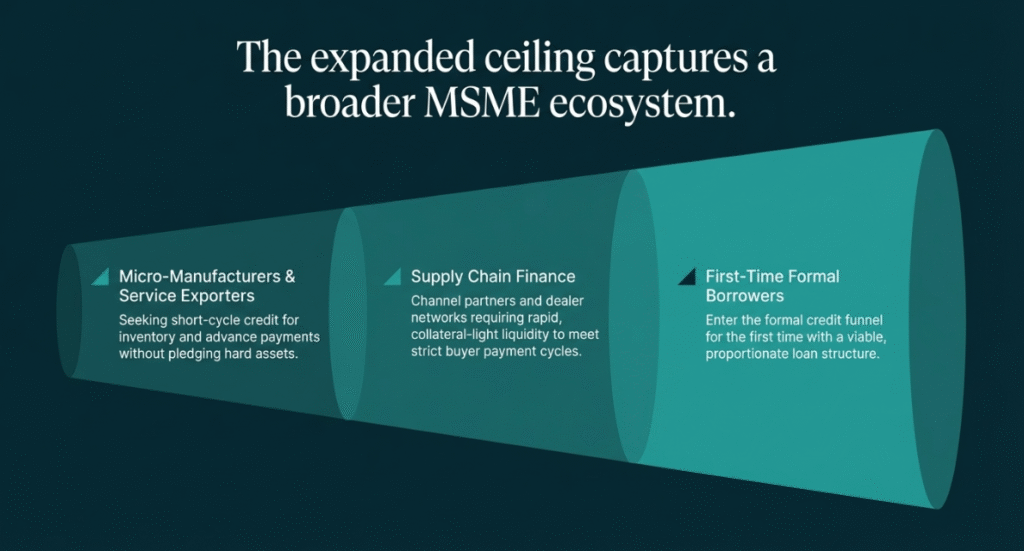

This matters across three immediate dimensions:

- Working capital access for micro-manufacturers and service exporters seeking short-cycle credit without pledging assets

- Supply chain finance positions where channel partners and dealer networks need rapid, collateral-light liquidity to meet buyer payment cycles

- First-time formal borrowers who previously fell outside the credit funnel now enter with a viable, proportionate loan structur