Structured Finance: When Plain Vanilla Debt Stops Working

A vanilla loan asks one question: can the borrower repay? Structured finance asks a sharper one: which specific cash flow, asset, or risk inside this business can we isolate and price on its own?

What Structured Finance Actually Is

Traditional debt prices your entire company. Structured finance prices a specific exposure within it.

That single shift unlocks four things plain vanilla debt cannot:

- Risk isolation — ring-fencing assets or cash flows from the rest of the business

- Risk tranching — the same exposure is sliced into senior, mezzanine, and junior pieces, each priced for its own risk appetite

- Credit enhancement — improving the rating of the senior piece through subordination, over-collateralization, or third-party guarantees

- Bespoke tenors and triggers — tenor, triggers, and repayment schedules match the actual life of the underlying cash flow, not a generic loan template

The 2026 Global Backdrop — Why It Matters Locally

Moody’s expects 2026 to be defined by stability at the aggregate level but meaningful divergence beneath the surface — performance differing by region, asset class, and origination channel rather than moving in lockstep.

Private credit growth is reshaping how assets are originated, putting pressure on traditional CLO collateral quality and altering issuance patterns for traditional ABS. S&P’s 2026 Global Structured Finance Summit flagged the same shift — macro uncertainty, evolving credit performance, and changing investor appetite across CLOs, private credit, fund finance, and APAC ABS/RMBS.

Translation for India: capital is available, but it’s increasingly flowing through structured channels rather than vanilla bank debt. The companies that learn to package their exposures will access it. The ones that don’t will pay 200–400bps more for the same money.

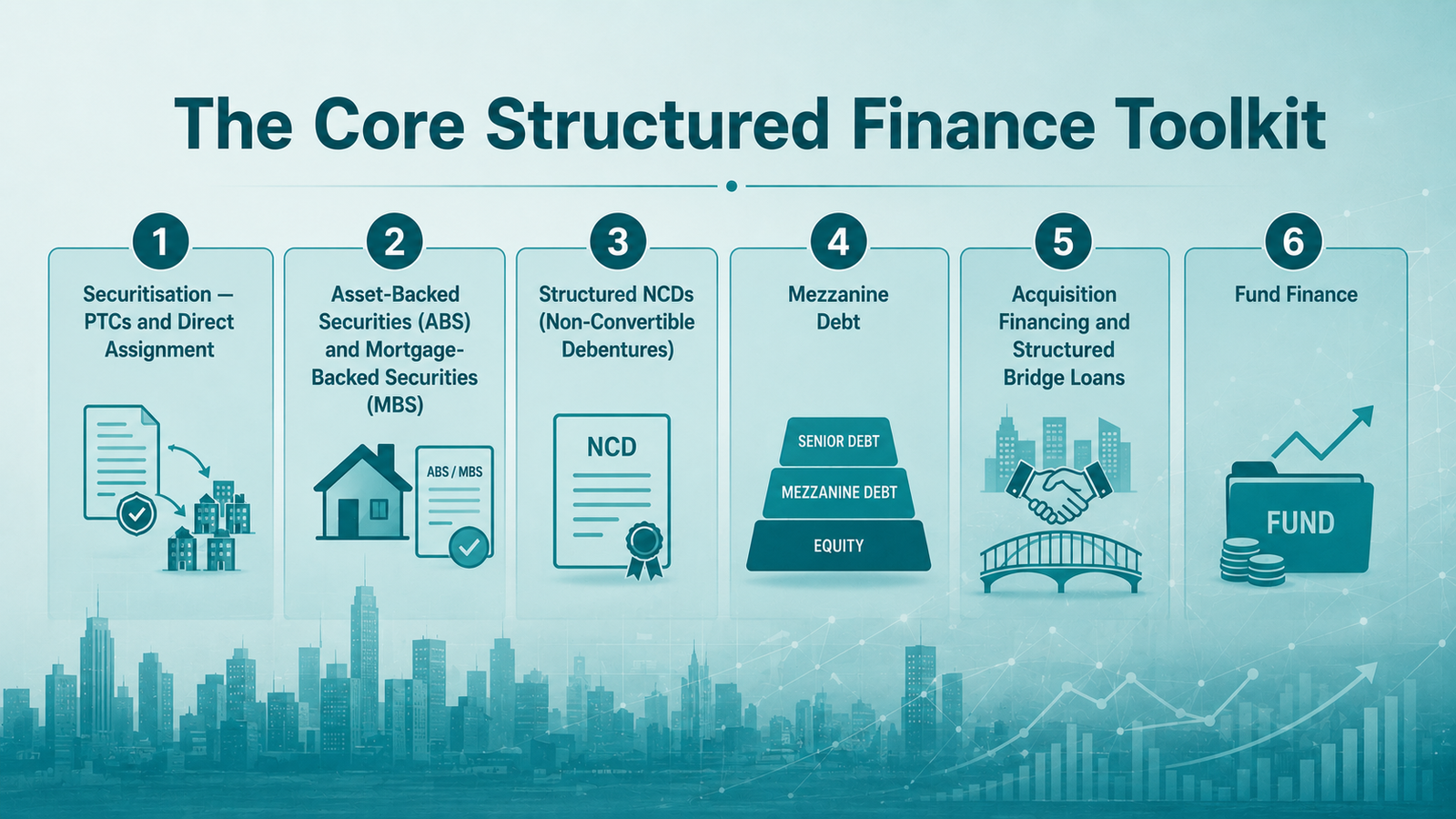

The Core Structured Finance Toolkit

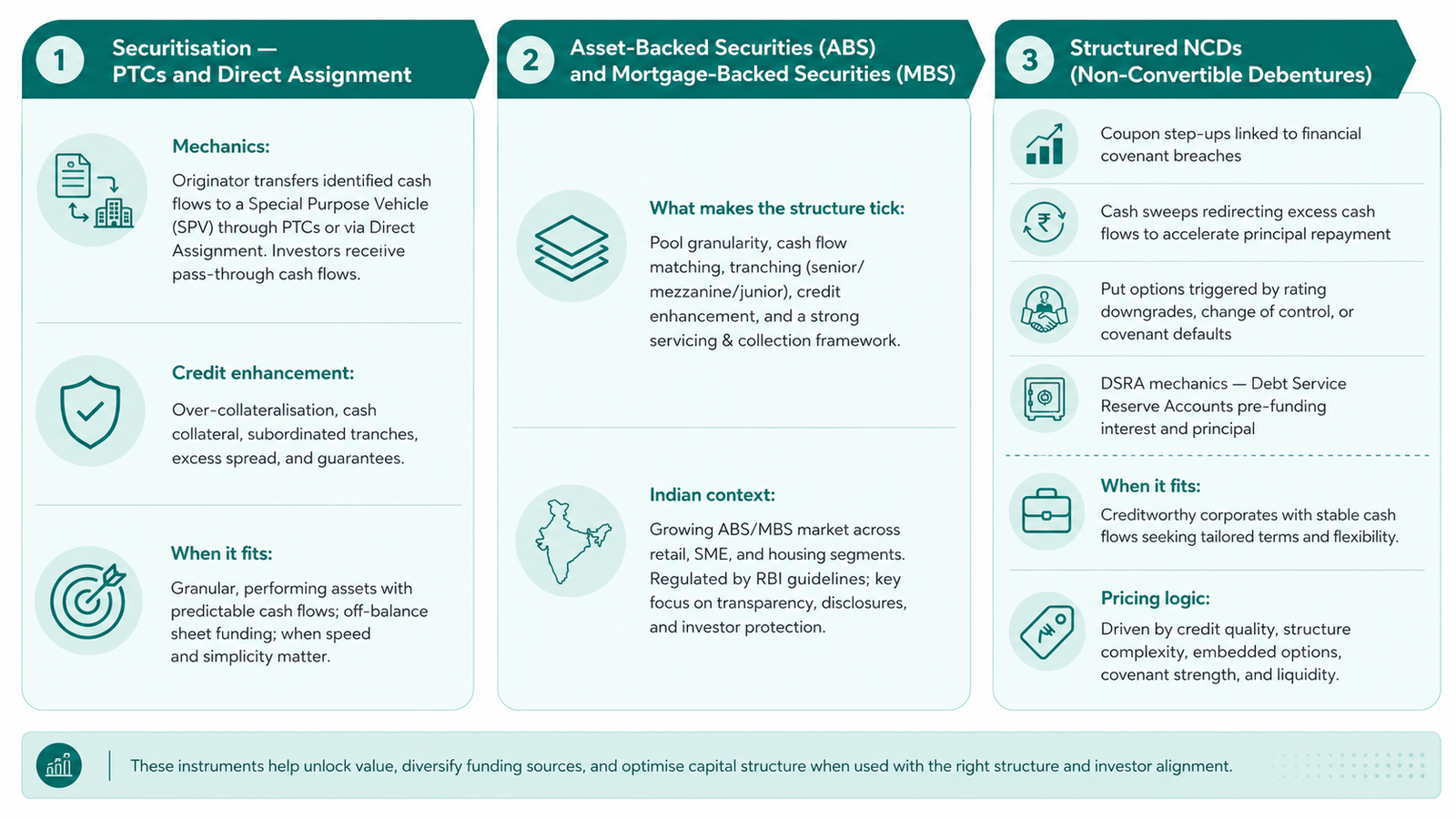

1. Securitisation — PTCs and Direct Assignment A pool of homogeneous receivables — typically loans, lease rentals, or trade receivables — is sold to a Special Purpose Vehicle (SPV). The SPV issues Pass-Through Certificates (PTCs) against this pool to investors.

Mechanics: Originator transfers the asset pool to SPV → SPV issues PTCs → investor receives pro-rata share of cash flows.

Credit enhancement: Typically 8–15% of pool value, via subordinated tranches, cash collateral, or over-collateralisation. The senior tranche routinely achieves AA+/AAA ratings even when the originator is rated A or below.

When it fits: NBFCs offloading retail loan portfolios, OEM captives monetising lease receivables, businesses with predictable, granular cash flows.

Direct Assignment is the simpler cousin — a bilateral sale of the asset pool to a single buyer (usually a bank meeting priority sector targets), without an SPV. Faster execution, narrower investor base.

2. Asset-Backed Securities (ABS) and Mortgage-Backed Securities (MBS)

Same principle as PTCs but typically larger, often listed, and with deeper investor participation. The underlying can be auto loans, gold loans, microfinance loans, equipment leases, or home loans.

What makes the structure tick: Bankruptcy-remote SPV, true sale of receivables, defined waterfall of cash flows, multiple tranches with explicit subordination.

3. Structured NCDs (Non-Convertible Debentures)

The workhorse instrument for Indian mid-market structured deals. An NCD with structural features that go far beyond a standard fixed-coupon bond:

• Coupon step-ups linked to financial covenant breaches

• Cash sweeps redirecting excess cash flows to accelerate principal repayment

• Put options triggered by rating downgrades, change of control, or covenant defaults

• DSRA mechanics — Debt Service Reserve Accounts pre-funding interest and principal

When it fits: Promoter funding, holdco-level financing, acquisition bridge debt, growth capital where equity dilution is unattractive.

Pricing logic: The structure determines the rating, the rating determines the coupon. A well-structured NCD with cash escrow and DSRA can price 150–250bps below an unstructured corporate loan to the same borrower.

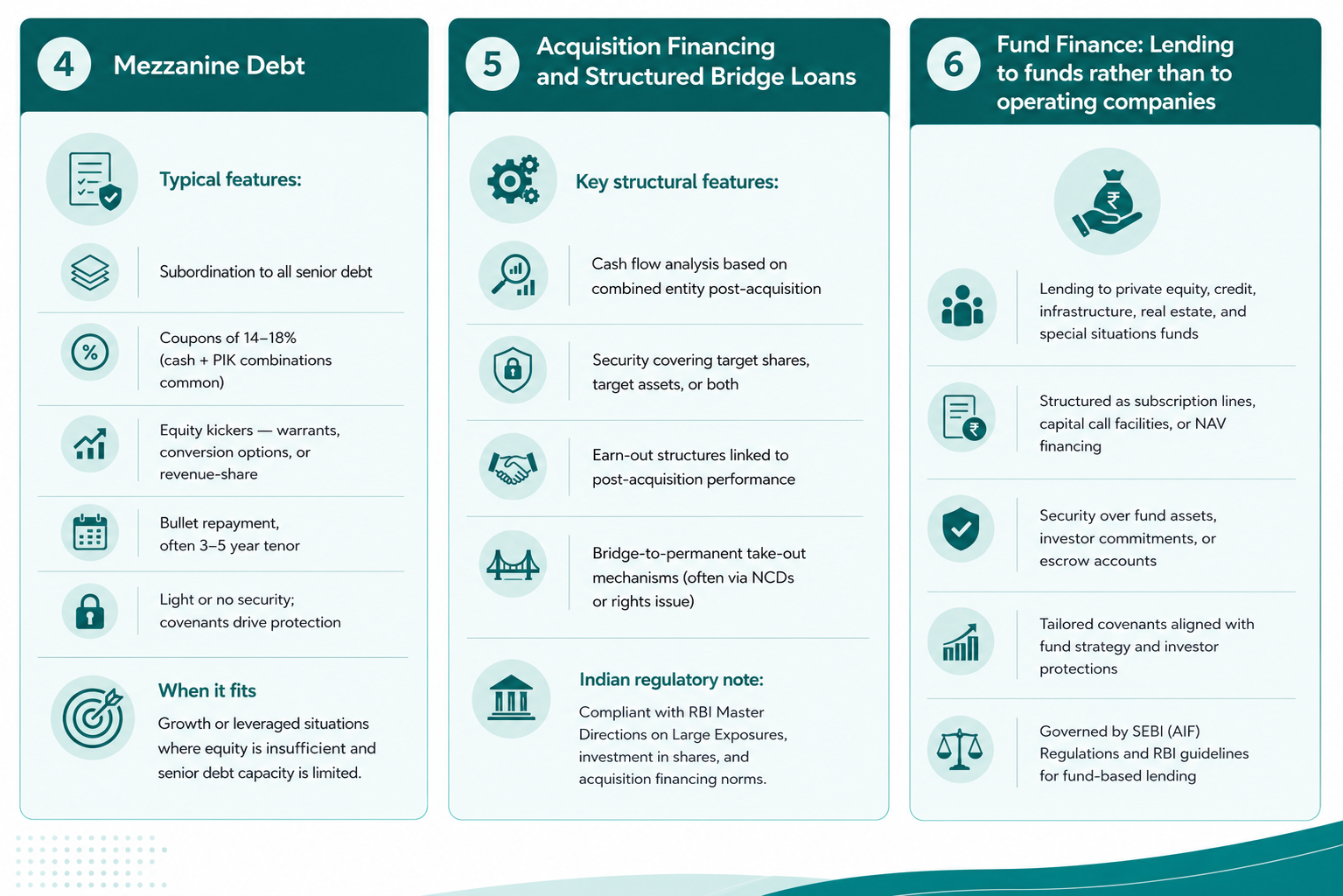

4. Mezzanine Debt

Subordinated debt that sits between senior secured debt and equity in the capital stack. Higher risk, higher return, structurally junior.

When it fits: Growth-stage companies with strong EBITDA but limited additional senior debt headroom, LBO funding, promoter buyouts, last-mile growth capital before an IPO.

5. Acquisition Financing and Structured Bridge Loans

Debt structured specifically around the cash flows and security of an acquisition target. Distinct from corporate debt to the acquirer.

6. Fund Finance

Lending to funds rather than to operating companies. The collateral is the fund’s underlying portfolio, unfunded commitments from LPs, or NAV.

Identified by S&P as one of the structurally growing segments in global structured finance.

Relevant when: PE/VC backed companies access NAV-based facilities through their sponsor’s fund line, indirectly improving the operating company’s effective cost of capital.

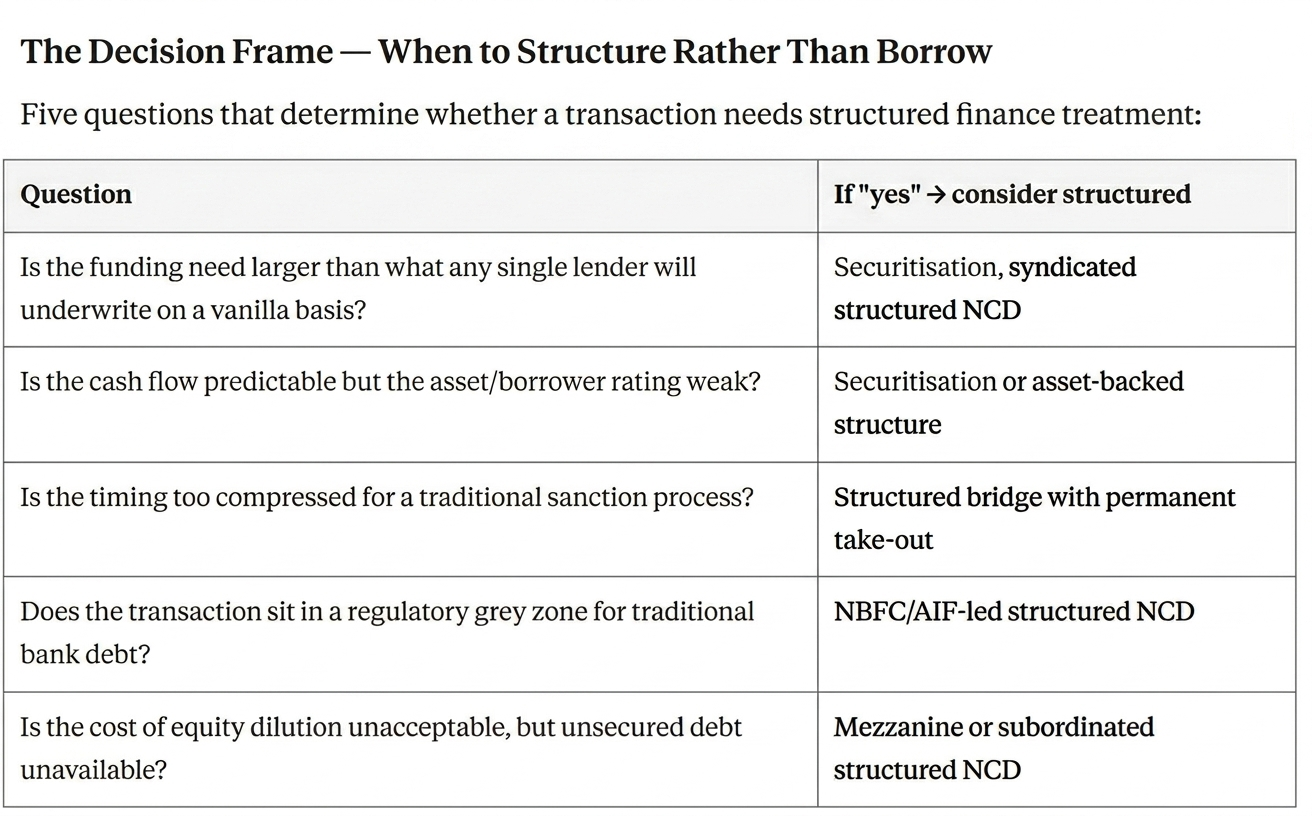

The Leverest Frame

We’ve structured these instruments from both sides — lender and advisor. Most of our deals begin with the same observation: the company isn’t short of capital, it’s short of the right structure.

Structured finance isn’t an alternative to traditional debt. It’s what you graduate to when traditional debt can no longer underwrite your specific situation.