The Real Problem Isn’t Liquidity. It’s Architecture.

In the same way, SIDBI pegs the MSME credit gap in India at roughly ₹30 lakh crore.

Delays in payments continue to strain working capital across sectors.

The default response remains the same: extend the CC limit with the primary bank.

A CC limit is familiar. Moreover, it’s priced as if every rupee of your working capital need has the same risk profile — which it doesn’t.

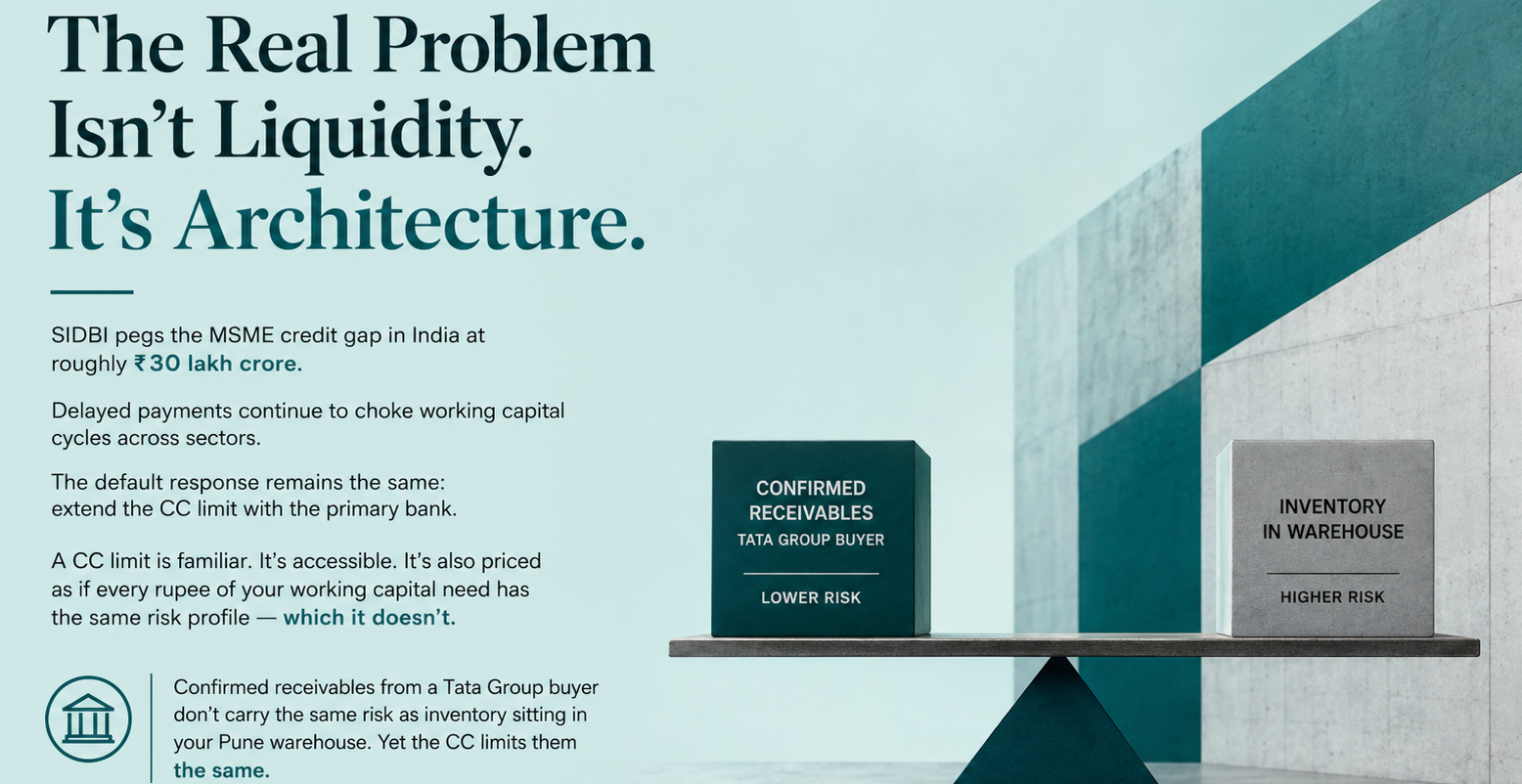

Confirmed receivables from a Tata Group buyer don’t carry the same risk as inventory sitting in your Pune warehouse.

Yet the CC limits them in the same way. That mispricing is what you’re paying for.

The Working Capital Toolkit — What Actually Exists

Most CFOs know these instruments by name. Few have stress-tested their own cash cycle against all of them. Here’s the working set:

1. Bill Discounting / LC-Backed Bill Discounting: For confirmed receivables backed by a bill of exchange. Tenor: 30–180 days. Typically, these: prices 50–150bps below CC for the LC-backed variant because the bank’s credit risk shifts to the LC-opening bank.

2. Invoice Discounting & Factoring (incl. TReDS) For short-cycle receivables from creditworthy buyers. TReDS is the RBI-regulated electronic platform where MSME invoices are auction-discounted. Tenor: 30–90 days. Pricing reflects the buyer’s credit rating, not yours — which is often a 200–300bps advantage for SMEs supplying to large corporations.

3. Channel Finance / Dealer Finance For ecosystems anchored to a large buyer or supplier. The anchor’s credit acts as the underwriting basis. Tenor: 60–120 days. As a result, it’s often unsecured at the dealer level because the anchor takes structural risk.

4.LC-Backed Lending / Buyer’s Credit — For input-heavy procurement, especially imports. In many cases, a buyer’s credit through an overseas branch can land at significantly cheaper rates than domestic INR funding, even after factoring in the cost of forex hedging. a Tenor: up to 1 year.

5. Export Credit (PCFC / Post-Shipment) For exporters. Notably, Pre-Shipment Credit in Foreign Currency (PCFC) is benchmarked to SOFR + spread — often 250–400bps cheaper than INR-denominated working capital.Tenor: typically 180 days.

6. Short-Term NCDs via NBFCs For revolving needs beyond bank appetite. In particular, this is useful for companies with strong cash flows but stretched bank exposure limits.

Sector by Sector — What Actually Fits

The “right” structure isn’t universal. It’s dictated by how cash moves through your business.

Manufacturing — Long Procurement, Inventory Heavy

The cash cycle: raw material procurement (often imported) → 45–90 day production cycle → 60–120 day receivables from OEMs.

The default mistake: stretching the CC limit to cover everything from steel imports to debtor financing.

The right architecture:

• First, LC + Buyer’s Credit for raw material imports (cheaper than CC, denominated risk)

• CC limit for inventory and in-process funding (which is what it was designed for)

• Bill discounting for confirmed OEM receivables (frees up CC limit headroom)

A mid-sized manufacturer with ₹50Cr of OEM receivables can typically free up ₹35–40Cr of CC headroom by moving to bill discounting, at a cost saving of 100–200bps on that portion.

Trading & Distribution — Velocity Over Margin

The cash cycle: thin margins, high turnover, dependence on supplier credit days vs. customer payment days.

The default mistake: treating every supplier and customer as homogeneous credit risk.

The right architecture:

• Vendor finance for procurement from large suppliers (the supplier gets paid early; you get extended credit terms)

• Channel finance for sales to anchored dealer networks

• Inventory funding for fast-moving stock, kept distinct from receivables financing

Consequently, distributors who segment their financing by counterparty rather than by need typically run 15–25% leaner on overall working capital.

Exporters — Currency Is a Financing Variable

The cash cycle: order → 45–60 day production → 30–90 day shipping and receivables.

The default mistake: funding the entire cycle in INR

The right architecture:

• PCFC (Pre-Shipment Credit in Foreign Currency) for production funding — benchmarked to global rates

• Post-shipment credit in foreign currency for receivables

• Export factoring for buyer-side risk transfer in new markets

Exporters who run their financing in the currency they invoice in often save 200–400bps on the working capital component alone, after hedging cost.

Early-Stage & Growth-Stage Companies — No Collateral, Real Receivables

The cash cycle: growth burn outpacing collections.

Instead, the default mistake is raising equity to fund what is actually a working capital need.

The right architecture:

• Invoice discounting against enterprise customer receivables

• Venture debt for non-dilutive runway extension

• Revenue-based financing for predictable subscription cash flows

• Funding a working capital gap with equity is one of the most expensive decisions a founder can make. The dilution cost compounds for years.

The Decision Framework

Before extending a CC limit, three questions are worth asking:

- What is the underlying asset or cash flow this funding is against? Receivable, inventory, import, or operational burn?

- Is there a counterparty whose credit is stronger than ours that we can structurally borrow against?

- Are we paying CC pricing for cash flows that deserve cheaper pricing?

If the answer to question 3 is yes — and for most growing SMEs, it is — you don’t have a working capital problem. You have a working capital structure problem.